The RTJ Bridge - The Research Platform Created by the Publishers of The RiskTech Journal

The RTJ Bridge is an independent research platform delivering institutional-grade IRM market intelligence, vendor competitive assessments, and strategic risk technology analysis. Built by the analyst who created the Integrated Risk Management category at Gartner, The RTJ Bridge gives risk leaders, technology executives, and solution providers the same caliber of competitive intelligence that major analyst firms charge $25,000 to $50,000+ per year to access.

Subscribers to The RTJ Bridge receive full access to:

IRM50 OnWatch Vendor Assessments — Competitive analysis of leading IRM vendors as market events unfold, covering platform strategy shifts, M&A impact, earnings signals, and positioning changes.

Autonomous IRM and AI Governance Research — Original research on how agentic AI is reshaping risk management operating models, from production deployment patterns to the structural implications for vendor platforms and enterprise programs.

Analyst Firm and Market Critiques — Independent assessments of research from Gartner, Forrester, and other major analyst firms, viewed through the IRM Navigator Model to identify gaps, validate signals, and challenge conventional positioning.

Board Governance and Audit Committee Intelligence — Research on oversight effectiveness, emerging risk response gaps, audit committee workload challenges, and the disconnect between risk reporting and executive action.

M&A and Strategic Alliance Analysis — Same-week analysis of acquisitions, partnerships, and PE investment moves reshaping the IRM competitive landscape, with implications for buyers, vendors, and investors.

Regulatory, ESG, and Sustainability Risk — Research on how evolving regulatory frameworks (SEC cyber disclosure, EU CSRD/CSDDD, AI regulation) affect enterprise risk programs and technology requirements.

IRM Navigator™ Market Intelligence — Strategic previews and deep dives from the IRM Navigator Model, the only independent model built specifically to evaluate integrated risk management maturity and vendor alignment.

Cyber Risk, Insurance, and Third-Party Risk — Analysis of cyber risk quantification, insurance market dynamics, and the convergence of third-party risk management into enterprise IRM programs.

Subscribe to get access now

The RTJ Bridge is an independent IRM research platform published by Wheelhouse Advisors. Subscribers receive ongoing access to vendor competitive assessments, AI disruption analysis, M&A and partnership impact research, and IRM Navigator™ market intelligence. This is the only research platform built and led by the analyst who created the Integrated Risk Management category, a market now valued at over $61 billion and projected to reach $133 billion by 2031.

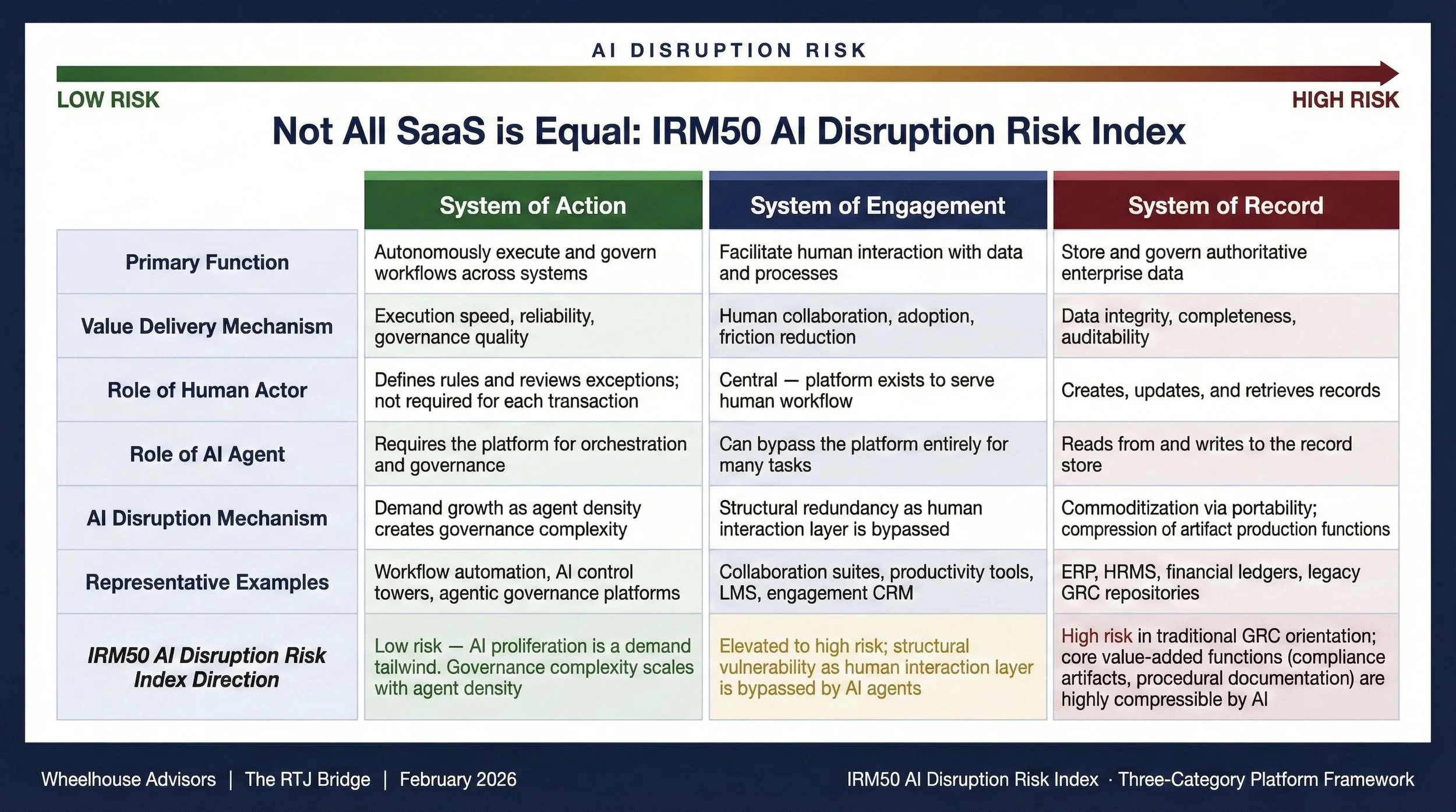

Not All SaaS Is Equal: IRM50 AI Disruption Risk Index

The enterprise software market is pricing AI disruption risk as if all SaaS platforms face the same structural threat. They do not. AI disruption risk varies fundamentally across platform categories based on architectural role, and the market's failure to distinguish between them is producing systematic mispricing. The IRM50 AI Disruption Risk Index introduces a three-category framework that makes those distinctions explicit, and the implications for capital allocation are significant.

The IRM50 AI Disruption Risk Index: Which Vendors Are More Durable in the Age of Autonomous IRM?

The IRM50 AI Disruption Risk Index covers the fifty vendors that define the IRM and GRC market: platform leaders like ServiceNow and Riskonnect, Big Four firms including Deloitte, EY, KPMG, and PwC, and specialized platforms like OneTrust, Archer, MetricStream, and AuditBoard. What sets this index apart is its methodology. Vendors are not ranked by market share or feature count, but by structural position across two dimensions that determine AI durability: compliance-artifact dependency and autonomous risk capability.

That distinction matters urgently right now. Global software stocks sold off sharply in February 2026 on AI disruption concerns. Morgan Stanley flagged downstream risk to the $1.5 trillion U.S. leveraged loan market. Blackstone now requires AI disruption risk assessment on the first two pages of every deal memo. Boards, executives, and investors who treat market leadership and structural durability as interchangeable are taking on risk they have not measured. This index measures it.

IRM50 OnWatch - One Year After Evolv, the Archer TRM Transition Is Still Playing Out

One year after Archer launched Archer Evolv as a next-generation, AI-powered SaaS offering, the most important signal for Technology Risk Management buyers is not the pace of feature announcements. It is the shape of the transformation Archer appears to be executing, and what that shape implies about where the TRM platform market is headed.

What NVIDIA’s CES 2026 Post Signals for Autonomous IRM

NVIDIA’s January 5, 2026, CES post is not “just a chip announcement.” It is a blueprint for making agentic systems cheaper to run, faster to execute, more distributed (from data center racks to desktops and edge), and more simulation-driven. For Autonomous Integrated Risk Management (Autonomous IRM), the practical implication is that the limiting factor shifts. It becomes less about whether the enterprise can afford the compute and more about whether it can manage autonomous decision loops with bounded execution, reliable orchestration, and audit-grade evidence.

What changed (and why executives should care)

Cadence shifts: more risk work can run continuously rather than quarterly because inference economics and long-context performance are improving.

Scope expands: autonomy moves beyond cyber and compliance into operational resilience and “physical” validation patterns that rely on simulation and long-tail testing.

Expectations rise: decision provenance and replayable evidence become baseline requirements, not premium features.

What follows is the translation of NVIDIA’s CES announcements into Autonomous IRM implications, using an executive pattern: signal, why it matters, implication, program design change, and a measurable buyer proof point.

The Static Quadrant: Why GRC Stopped Moving

The “2025 Gartner® Magic Quadrant™ for Governance, Risk and Compliance (GRC) Tools, Assurance Leaders” offers more than an update on vendor positioning. It captures a defining moment in the evolution of enterprise risk management technology. For the first time since Gartner began coverage of this market in 2008, the Visionaries quadrant is completely empty.

This absence is not an error or a symptom of decline. It is a reflection of structural maturity and the point at which a technology category stops expanding outward and begins to integrate inward. The GRC segment has stabilized around its purpose: to deliver reliable assurance, compliance automation, and control verification at scale.

This research note is a follow-up to the recent RiskTech Journal article, GRC Without Visionaries: What the 2025 Gartner® Magic Quadrant™ Reveals About the Future of Risk. It further examines why the quadrant has gone static, why that matters, and how the integration of GRC within the broader Integrated Risk Management (IRM) model marks a necessary and healthy progression. It concludes that the current stillness in GRC represents not the end of innovation, but the beginning of Assurance Intelligence. It is the fusion of compliance evidence, operational data, and AI-enabled assurance that will define risk management by 2032.

Agentic AI Moves From Hype to Operating Model: What Risk Leaders Must Do Now

EY’s newest global insight, “What Risk Leaders Need to Do Now About Agentic AI,” sets a clear challenge: organizations that treat agentic AI as another productivity initiative risk amplifying exposure, not mitigating it. The report argues that risk functions must now move beyond experimentation and build an enterprise operating model where autonomous and semi-autonomous agents can act safely, transparently, and in alignment with strategy.

This message reinforces a structural shift already underway in Integrated Risk Management (IRM). Wheelhouse Advisors’ Autonomous IRM model defines how these agentic systems should operate—not as isolated bots or chat interfaces, but as integrated decision engines that connect strategic intent, operational execution, and assurance validation.

Workiva’s Q3 2025 Results Signal the Rise of “Assured Data Platforms” in the IRM Market

Workiva’s Q3 2025 results represent more than a financial beat—they reveal a strategic inflection point for the Integrated Risk Management (IRM) market. The company delivered total revenue of $224 million, up 21% year over year, with subscription and support revenue growing 23%. Its non-GAAP operating margin expanded to 12.7%, nearly tripling from the prior year. Just as significant, customers with annual contract value (ACV) above $500,000 rose 42%, confirming enterprise-scale adoption of Workiva’s unified disclosure and assurance platform.

This growth underscores a broader market movement toward “assured data platforms”—solutions that unify financial, sustainability, and risk reporting within one governed architecture. As ESG regulation, audit digitization, and AI assurance converge, Workiva’s performance signals what IRM leaders should expect across the next phase of market maturity.

Agentic Operational Risk: How AI Is Reshaping Control, Performance, and Resilience

Operational risk management is evolving from reactive oversight to intelligent orchestration. Agentic AI, systems that can plan, tool, and act with bounded autonomy, is at the center of this shift. These agents compress cycle times, expand control coverage, and deliver evidence with audit grade traceability. Within the IRM Navigator™ Model, they strengthen the connection between Performance and Resilience, the two objectives where ORM delivers the most tangible value.

The Risk Ignored, Part II Chapter 5: The Academic Reckoning

In Part I of The Risk Ignored, we followed the rise and fall of GRC. Born in the aftermath of the Sarbanes-Oxley Act, it was codified by Archer, PwC, and Michael Rasmussen, and quickly became the acronym that defined a market. Yet by the late 2000s, GRC was collapsing under its own weight. The very acronym that promised coherence came to mean everything and, in practice, nothing at all.

The story of The Risk Ignored Part II: The Seeds of Integration begins here. The collapse of GRC and the inadequacy of compliance-first ERM created a void. The question, for both scholars and practitioners, was what comes next.

Workiva’s Q2 Surge Underscores IRM Integration Strategy

Workiva’s second quarter 2025 results reaffirmed the company’s strategic pivot toward an integrated risk and compliance platform, highlighting a promising yet incomplete transformation. The company delivered robust 21% year-over-year revenue growth, driven by strong subscription growth (up 23%), sparking a noteworthy 32% post-earnings stock surge. This positive investor reaction underscores early confidence in Workiva’s evolution from a compliance-centric financial reporting tool toward broader capabilities encompassing ESG, audit, financial disclosure, and integrated risk management (IRM).

Identity's Moment of Reckoning: What Palo Alto Networks' Acquisition of CyberArk Means for the IRM Market

Palo Alto Networks announced the strategic acquisition of identity security leader CyberArk for approximately $25 billion on July 30, 2025, reshaping the competitive landscape for Integrated Risk Management (IRM). Leveraging insights from Wheelhouse’s proprietary IRM Navigator™ Model and the IRM Navigator™ Viewpoint Report (2025 Edition), this note analyzes critical implications for IRM, IRM-adjacent, and legacy Governance, Risk, and Compliance (GRC) providers. IRM vendors and service providers must decisively respond to accelerating consolidation trends driven by cybersecurity leaders expanding into integrated risk management domains.

NAVEX’s Big Deal: Goldman Sachs and Blackstone Bet on IRM

The July 2025 agreement for a Goldman Sachs-led consortium to acquire a majority stake in NAVEX marks a milestone for the Integrated Risk Management (IRM) technology market¹. Long viewed as a niche segment, IRM tech is now receiving institutional validation on a grand scale. With Goldman Sachs Alternatives and Blackstone joining forces—alongside BC Partners retaining a minority stake and Vista Equity Partners fully exiting—the deal signals that IRM software has firmly come of age.

From a high-level thesis perspective, the NAVEX acquisition conveys institutional confidence in the long-term growth of IRM. It suggests that large-cap investors believe the market will continue consolidating and expanding, with platforms like NAVEX One poised to capture increasing enterprise spend. The participation of firms like Goldman and Blackstone is more than just capital—it is an endorsement of the market’s strategic relevance, particularly as organizations face rising regulatory obligations, complex supply chains, and evolving digital risks.

Why Q1 2025 Was a Wake Up Call for Compliance-Centric IRM Vendors

Despite beating earnings estimates, a surprise sell-off in Workiva stock on May 2 sent a jolt through the Integrated Risk Management (IRM) technology market. The trigger wasn't financial underperformance but political indecision: Germany and France signaled their intent to water down or delay the European Union's Corporate Sustainability Reporting Directive (CSRD) application. In addition, the European Parliament formally agreed to postpone the enforcement of new sustainability and due diligence rules.

The reaction was swift and severe for Workiva, a leading compliance-first vendor built around ESG reporting and assurance workflows. However, this moment revealed a more systemic truth for the broader IRM market: IRM's trajectory is now shaped as much by the pace of regulatory implementation as by the innovation of its technology platforms.

The market's reaction reflects a correction in growth expectations for compliance-oriented vendors and an inflection point in how investors, boards, and buyers view risk management software. As regulation stalls, the IRM market is fragmenting into more clearly defined value segments—each responding differently to volatility. These are the market realities shaping Q1 2025.