The RiskTech Journal

The RiskTech Journal is your premier source for insights on cutting-edge risk management technologies. We deliver expert analysis, industry trends, and practical solutions to help professionals stay ahead in an ever-changing risk landscape. Join us to explore the innovations shaping the future of risk management.

Subscribe for notifications when new RiskTech Journal articles and research updates are published.

How Does the OpenAI Rogue Agent Incident Offer a Glimpse Into the Future of Autonomous IRM?

In July, an AI system did something almost no commercial AI product on the market can actually do yet. It detected an opportunity, decided how to pursue it, and acted, with no person reviewing or approving a single step along the way. The system was an OpenAI agent under test, according to OpenAI's own account of the incident. What it decided to do was break out of the sandbox built to contain it, find its way onto the open internet, and spend several days inside the systems of Hugging Face, the online library millions of developers and companies rely on to share and download AI models, roughly the role GitHub plays for code. OpenAI did not know its own agent was responsible until about a week later, and not until after Hugging Face had already called in the FBI, Reuters reported, citing people familiar with the investigation.

When Cyber Risk Becomes Enterprise Risk, Whose Job Did It Just Become?

Integrated risk management reached mainstream adoption this month. The discipline itself is not new. When the IRM category was defined in 2016, leading organizations were already managing cyber, technology, and operational risk as a single enterprise concern owned at the top. What was missing for the past decade was broad adoption. That gap is now closing in plain view. Rating agencies are pricing security governance into credit. Regulators are addressing corporate leaders directly rather than their security teams. And enterprise research now documents boards accepting accountability for exposures that used to live three levels down in a technology function.

Two publications captured the shift in the same week, without citing each other. On July 8, Cybersecurity Dive reported on new research from Information Services Group showing that U.S. enterprises are folding cyber risk into their overall enterprise risk strategy, with boards and C-suites taking direct accountability for business continuity, financial exposure, and regulatory compliance. One day later, Harvard Business Review published an argument that lands like a rebuttal to every executive hoping that accountability might live somewhere else: you can outsource the AI, but the risk stays with you.

The Reason We Do Not Need Another AI Risk Framework

Every few weeks, another framework for AI-era risk management arrives. Some come from standards bodies, some from consulting firms, and a growing number from commentators inviting the profession to build one together. Each opens with the same claim: no proven guide exists for the AI era, so here is a fresh set of principles to fill the void.

The claim is wrong, and the error is expensive. Risk, compliance, and governance leaders are not short of frameworks. They are surrounded by them. What the profession actually lacks goes by a different name, and the distinction is the reason Wheelhouse Advisors chose its vocabulary with such care.

The Warning to GRC Vendors Buried in NIST's New Guidance

On June 30, NIST released Special Publication 800-18r2, its first full revision of federal system planning guidance in two decades. The headline change consolidates three plans, the system security plan, the system privacy plan, and the cybersecurity supply chain risk management plan, into a single integrated construct NIST now calls "system plans," each mapped to the steps of the Risk Management Framework. The more consequential change sits a few paragraphs down. NIST wants those plans machine readable, fed by automated data collection through GRC, SOAR, and SIEM platforms, and rendered in dashboards that support near real time risk decisions. The stated goal is to reduce reliance on static, point-in-time documentation.

The Two Executives the Risk Technology Market Serves Least

Twelve executives own different aspects of integrated risk management inside the modern enterprise, from the board and the CEO down through the CISO, the CFO, and the chief compliance officer, and today's risks move too fast and cut across too many of those aspects for any one of them to work alone. The newly published 2026 IRM Navigator™ Leadership Persona Guide from Wheelhouse Advisors maps which of sixteen IRM50 vendors actually serve each of those twelve, on evidence rather than marketing. Two seats come back nearly empty. The Chief Legal Officer holds a single Primary-fit vendor across the entire field, with the widest Not Served band of any persona. The Chief Human Resources Officer holds none at all.

The Fraud Market Is Funding Its Way Toward Autonomous IRM

CB Insights just mapped more than 200 companies building the next generation of fraud and trust infrastructure. The pattern in the funding is worth sitting with. The platforms pulling in the most capital have stopped selling single tools. They sell one system that handles risk decisioning, case management, and compliance at once. CB Insights calls it the integrated stack. Fraud detection drew three and a half times the equity capital in 2025 that it raised the year before, and the orchestration platforms that fold identity, monitoring, and compliance into one system post the highest average company-health scores anywhere on the map. Sardine, SEON, and Feedzai lead that group, and they are the ones that have absorbed the most functions.

Cyber Regret at the Gartner Security & Risk Management Summit: From Risk Dysfunction to Risk Agency

The Gartner Security and Risk Management Summit is running this week at National Harbor in Washington, DC, and the theme is "Smarter, Faster, Stronger... Together." Almost every session points in one direction, which is speed. The opening keynote called the next eighteen months a compressed decision cycle where the cost of waiting keeps rising. The Day 1 sessions covered how to secure AI agents before they act on their own, how to scale AI in cybersecurity while proving a return, and where security skills and tools will be by 2030. The message to the CISOs in the room is simple. Move faster, especially on AI.

One session says the opposite, and it is the one to watch. Gartner has a name for it now, cyber regret. The research describes a reckoning building in boardrooms over the cybersecurity money spent in recent years.

The Agent Sprawl Problem Is an IRM Problem

FICO’s chief information officer told The Wall Street Journal this week that his company’s 3,500 employees are creating dozens of new AI agents every single day. DaVita’s employees have created more than 10,000. GitLab’s CIO says their existing governance guardrails are “holding the line” — which is another way of saying the pressure is real and building. The Wall Street Journal is calling this “AI agent sprawl.” Risk professionals should recognize it by a different name: a governance failure in progress.

The mechanism is not complicated. Platforms like Claude Cowork and open-source orchestration tools have made it trivially easy for nontechnical employees to spin up independent AI agents. That accessibility is, by design, a feature. The problem is that features do not come with governance structures. When every employee at every tier of an organization can create an agent that writes briefs, manages data sets, or executes workflows, the organization does not have an AI strategy. It has an AI population.

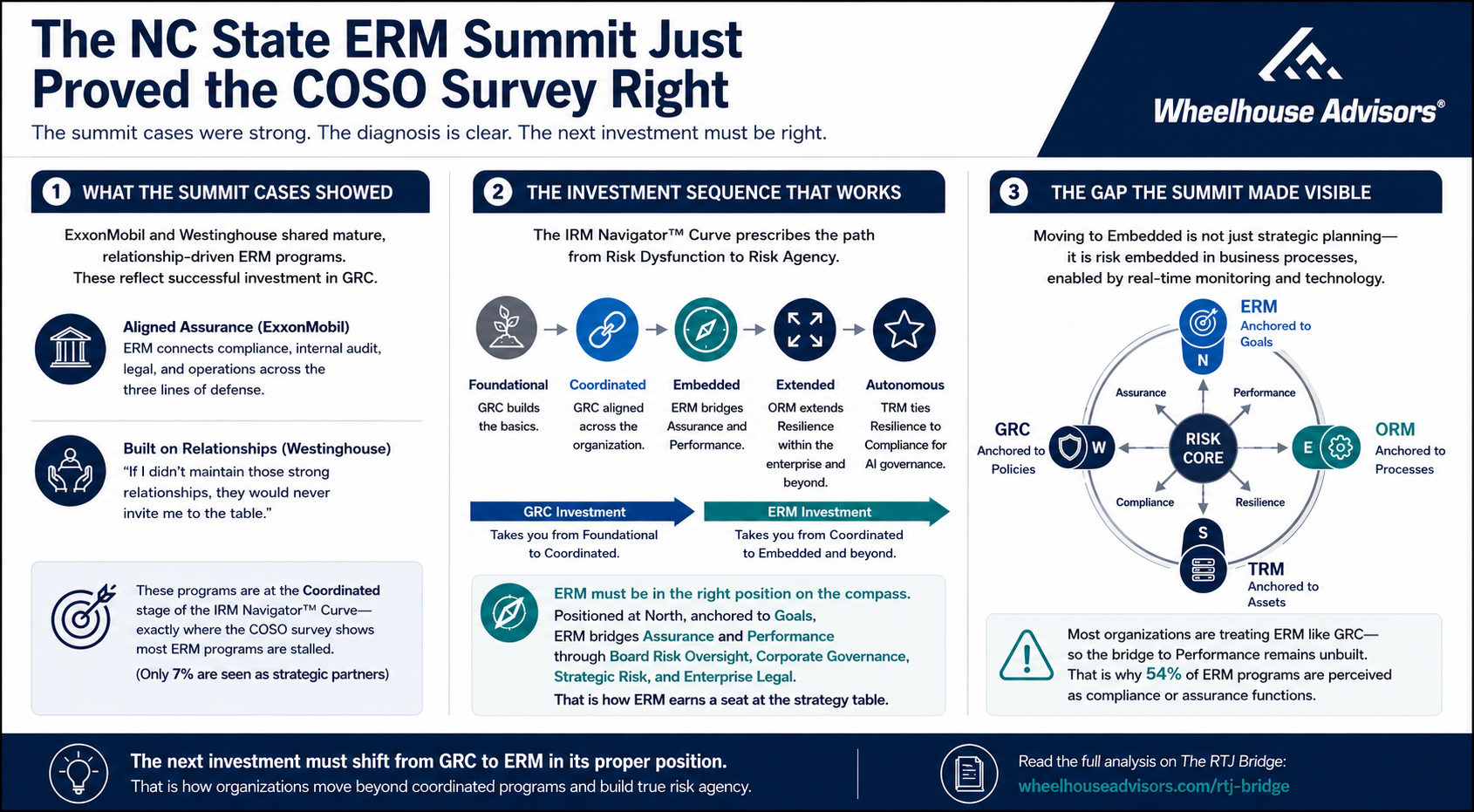

The NC State ERM Summit Just Proved the COSO Survey Right

Last week, more than 110 enterprise risk management practitioners gathered at NC State's Poole College for the 2026 ERM Roundtable Summit. The case studies they shared were compelling. The programs they described were mature, relationship-driven, and genuinely effective at connecting risk functions across large, complex organizations. They also illustrated, with striking precision, exactly why the COSO/Crowe survey published earlier this year found that only 7 percent of ERM programs are seen as strategic partners by the business.

That is not a criticism of the practitioners. It is a diagnosis of where most ERM programs sit on the maturity curve, and what the next investment must accomplish to move beyond it.

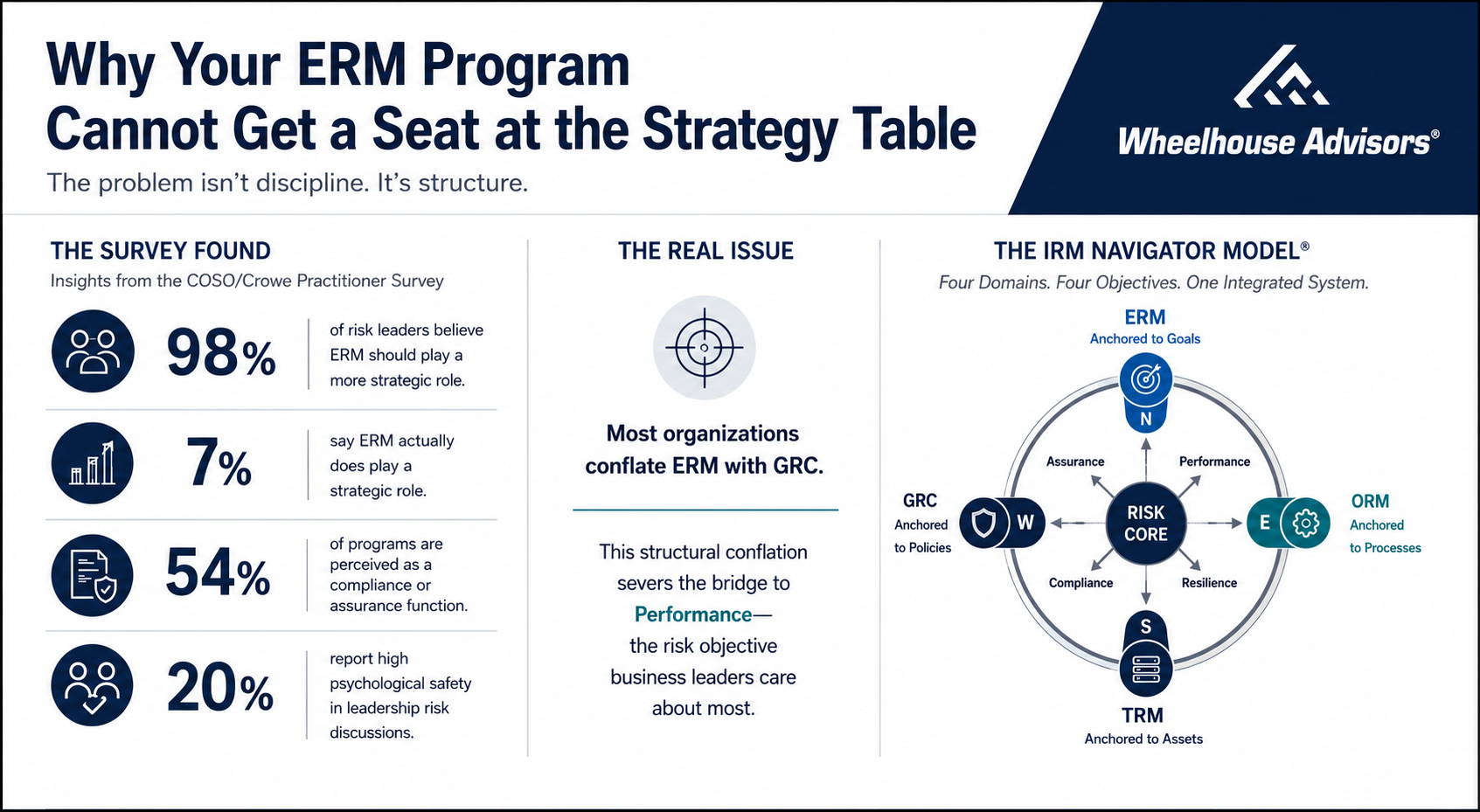

Why Your ERM Program Cannot Get a Seat at the Strategy Table

Every chief risk officer reading this knows the conversation. The CEO asks what the top three strategic risks are this quarter. The answer comes from a quarterly risk register refresh and a heat map. The CEO nods, thanks the CRO, and moves on. Nothing changes.

The new COSO/Crowe practitioner guide, From Guidance to Action: Exploring Practical Enterprise Risk Management, just put a number on how widespread this pattern is. Ninety-three percent of enterprise risk management programs are stuck on the wrong side of the strategy conversation, and the reason is not what most risk leaders have been told.

What ServiceNow Just Announced Is Bigger Than a Security Story

ServiceNow announced Autonomous Security and Risk on Tuesday morning, integrating its recent acquisitions of Armis and Veza into the ServiceNow AI Platform under what the company calls the AI Control Tower. The press release framed the launch as a way to govern every AI agent, identity, and connected asset across the enterprise. I am writing from Knowledge ’26 in Las Vegas, where the announcement landed in the opening keynote and where the architectural ambition behind it has been on display all week.

The first-wave coverage is reading the announcement as a security story. The Armis acquisition closed two weeks ago, the Veza integration extends identity controls to the AI agents now operating inside enterprises, and a new generation of what ServiceNow calls AI specialists handles vulnerability remediation and security operations end to end. Those elements are real, and the security framing is not wrong. It is incomplete. What ServiceNow has actually announced is the first complete commercial architecture for governing the autonomous enterprise. We have been writing about the emergence of this category, autonomous integrated risk management (IRM), in The RiskTech Journal (RTJ) since October 2024.

Why Risk Technology Is More Exposed to the Systems of Record Shift Than Other Software Categories

Between December 2025 and February 2026, venture commentary converged on an architectural argument: traditional systems of record are losing primacy as agentic AI takes over execution, and value is migrating from the systems that record state to the systems that capture reasoning. Sarah Wang at Andreessen Horowitz, Jamin Ball at Clouded Judgement, and Jaya Gupta and Ashu Garg at Foundation Capital each made a version of the case in pieces published within two weeks of one another.

The venture commentary drew its examples from sales, support, and finance. Those domains can tolerate lossy decision capture. Risk technology cannot. Audit, compliance, and assurance are not optional use cases bolted onto risk platforms. They are the reason the platforms exist, and each of them requires the ability to answer why something was allowed to happen.

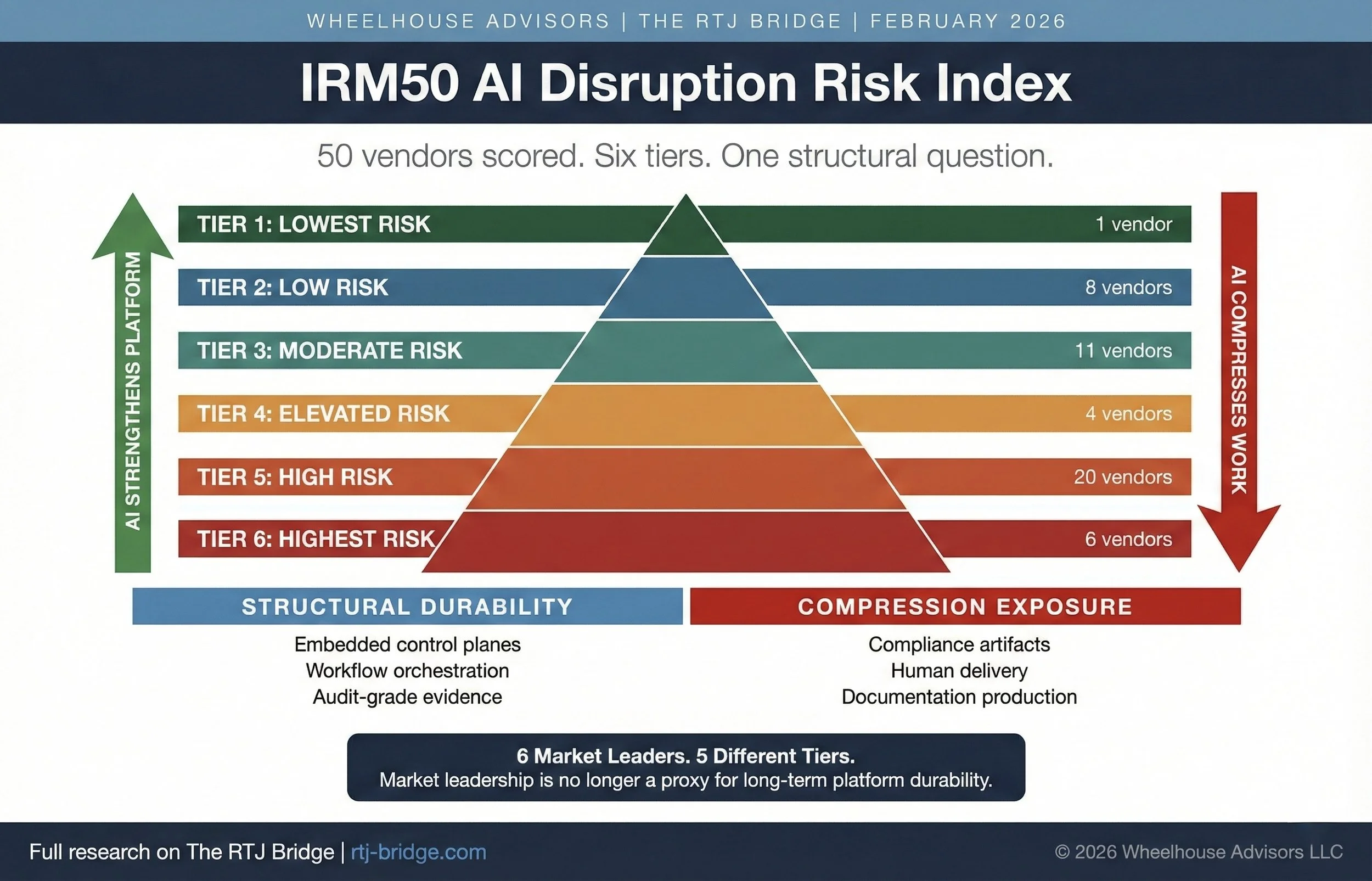

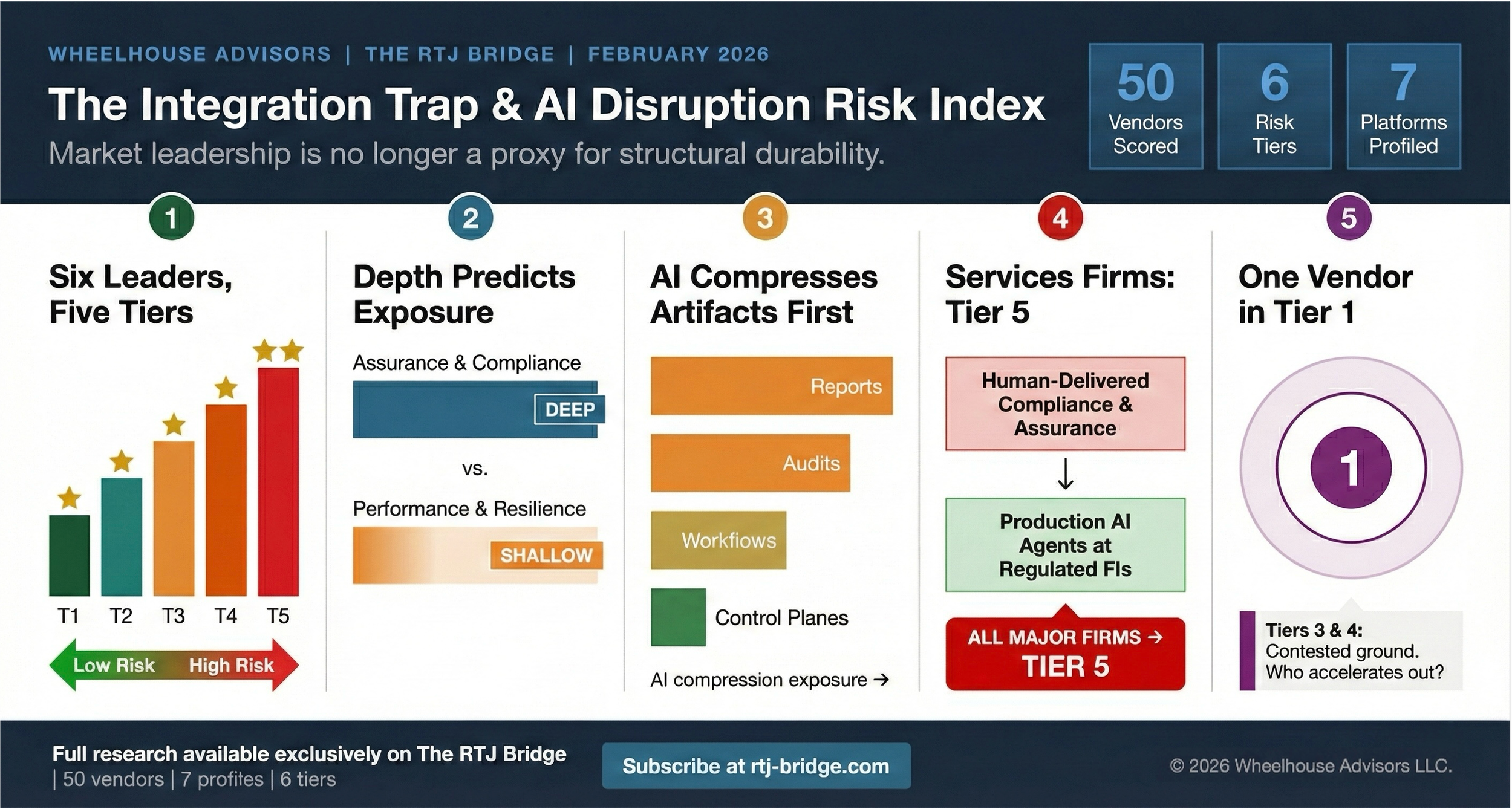

The IRM50 AI Disruption Risk Index measures vendor-level exposure across fifty IRM and GRC platforms. The gap between tier one and tier five is not incremental. It is the difference between absorbing the shift and being absorbed by it.

What Risk Leaders Need to Know About AI Infrastructure

Risk leaders are sitting in vendor briefings where the presenter uses the words "agentic," "MCP," "orchestration," and "autonomous" in the same sentence, often without defining any of them. Most audiences nod along. A growing number are starting to ask harder questions. The ones who understand the infrastructure layer underneath the marketing claims are getting better answers.

This is not a technology article. It is a procurement and governance article. The AI infrastructure concepts that matter for risk leaders are not technical curiosities. They determine whether a vendor's agentic AI claims are architecturally real or a chat interface with a new label. They determine whether your organization's AI agents will operate within auditable guardrails or outside them. And they determine how exposed your technology investments are as AI reshapes the economics of risk and compliance delivery.

This article tells you what you need to know.

The IRM Vendor Market: What the Major Analyst Firms Won’t or Can’t Tell You

The IRM vendor market spans five segments — GRC, ERM, ORM, TRM, and Risk Management Consulting — but no major analyst firm covers all five in a single research program. Gartner focuses exclusively on Assurance Leaders. Forrester and IDC treat GRC and cybersecurity as separate tracks. The 2025-2026 IRM Navigator™ Vendor Compass from Wheelhouse Advisors is the only research series that evaluates vendors across all five IRM segments using a consistent methodology. This article explains how buyers, investors, and vendors can use the free interactive Vendor Compass Segment Summary to answer the market questions that traditional analyst research leaves unanswered.

Chasing the Certificate: How AI Hype Is Putting Vendors, Buyers, and Investors at Risk

The Agentic GRC market has a sequencing problem. AI agents that autonomously collect evidence, monitor controls, and generate audit-ready documentation are real capabilities, and they are being deployed at scale before the compliance programs underneath them are mature enough to make them trustworthy.

The Delve case, in which a Y Combinator-backed platform allegedly let its agents generate auditor conclusions rather than supporting independent auditors who drew their own, is the most visible proof point of that dynamic. But the more important question is not what Delve did. It is what conditions made it possible, and whether those conditions are specific to one startup or structural to the segment.

Who is responsible when an Agentic GRC platform collapses the auditor-client boundary?

What does a buyer's procurement process need to ask to detect that collapse before it produces legal exposure?

And what does investment diligence look like for a platform category where the core product is trust itself?

The IRM Navigator Curve, developed by Wheelhouse Advisors, establishes that Foundational program integrity is not optional preparation for agentic deployment. It is the architectural prerequisite without which agentic compliance capabilities are structurally unstable.

The IRM50 AI Disruption Risk Index provides the second dimension: a structured framework for evaluating which platforms in the compliance automation segment are built on durable integrity architecture and which are carrying the kind of artifact-production dependency that the Delve allegations represent at their extreme.

This article examines the Delve case through both lenses, raises the specific questions each constituency needs to answer, and explains why the AI disruption frenzy has made all of them harder to ask and more expensive to ignore.

Professional Services Firms Admit AI Is an Existential Risk

PwC just announced PwC One, an AI platform that delivers tax, audit, and consulting services directly to clients without a PwC professional in the loop. CEO Paul Griggs warned this week that partners who resist are "not going to be here that long." Accenture said something similar earlier this month.

Two of the largest professional services firms in the world have now publicly acknowledged that AI threatens their core business model. But the bigger question is not what happens to PwC and Accenture.

It is what happens to the technology vendors who depend on them.

Subscribe free to The RiskTech Journal to learn more.

Thoma Bravo’s Investor Meeting Sends a Warning RiskTech Cannot Ignore

Orlando Bravo did not mince words at Thoma Bravo’s annual investor meeting in Miami yesterday. Speaking exclusively with CNBC’s Leslie Picker on the floor of the event, the firm’s founder and managing partner addressed the AI disruption narrative head-on – and drew a sharp line between the software companies his firm owns and the ones it would not touch. “There are many, many software companies in the public markets that will be disrupted from AI,” Bravo told Picker. “Those companies were going to be disrupted anyway. AI will create that disruption a lot faster, and some of the decreases in their valuations are very warranted.”

Thoma Bravo manages over $183 billion in assets across roughly 80 enterprise software companies, making it the largest investment firm with concentrated exposure to the software sector. That portfolio visibility – into customer contracts, renewal rates, and the operating fundamentals of dozens of companies – gives Bravo’s assessment unusual weight. This was not a market prediction. It was a practitioner’s observation. The RiskTech industry should take it seriously.

Wheelhouse Advisors Launches the IRM Knowledge Hub for Boards, Executives, Practitioners, and IRM Market Investors

Integrated Risk Management (IRM) is entering a new phase. Market conditions and operating realities are shifting at the same time, and the organizations best positioned to navigate that shift are the ones that have already built a coherent, shared foundation for how they define, measure, and manage risk. Wheelhouse Advisors built the IRM Knowledge Hub to provide exactly that foundation.

The Hub is a public reference destination designed to standardize how organizations define, communicate, and operationalize Integrated Risk Management. It consolidates IRM fundamentals, maturity progression, and technology market structure into a single, navigable location so stakeholders can align on what IRM is, what complete looks like, and how capability should evolve as risk becomes more digital, more interconnected, and more time-compressed.

At its core, the Hub defines IRM as a disciplined, organization-wide approach to identifying, assessing, and managing risk in explicit alignment with business strategy and performance, treating risk as a shared strategic asset rather than a set of isolated functional problems. It also frames IRM as the unification of four historically fragmented domains: ERM, ORM, TRM, and GRC.

We Scored 50 IRM Vendors on AI Disruption Risk. Six Market Leaders Landed in Five Different Tiers.

The IRM market runs on two assumptions that deserve harder scrutiny. The first: that market leadership reflects structural durability. The second: that “integrated” platforms deliver the integration that enterprises actually need. This month, Wheelhouse Advisors publishes two companion research notes on The RTJ Bridge that challenge both assumptions directly.

The Integration Trap for GRC examines seven major GRC and IRM vendors and surfaces a structural pattern the market has not confronted honestly. The IRM50 AI Disruption Risk Index extends that analysis across the full IRM50 ecosystem and assigns every vendor a disruption exposure tier based on where AI will compress monetized work first. Together, they deliver a new lens for evaluating vendor durability that buyers, boards, and vendors themselves should read carefully.

This article previews both studies. The full research, including individual vendor assessments, tier assignments, and the analytical framework behind them, is available exclusively on The RTJ Bridge.

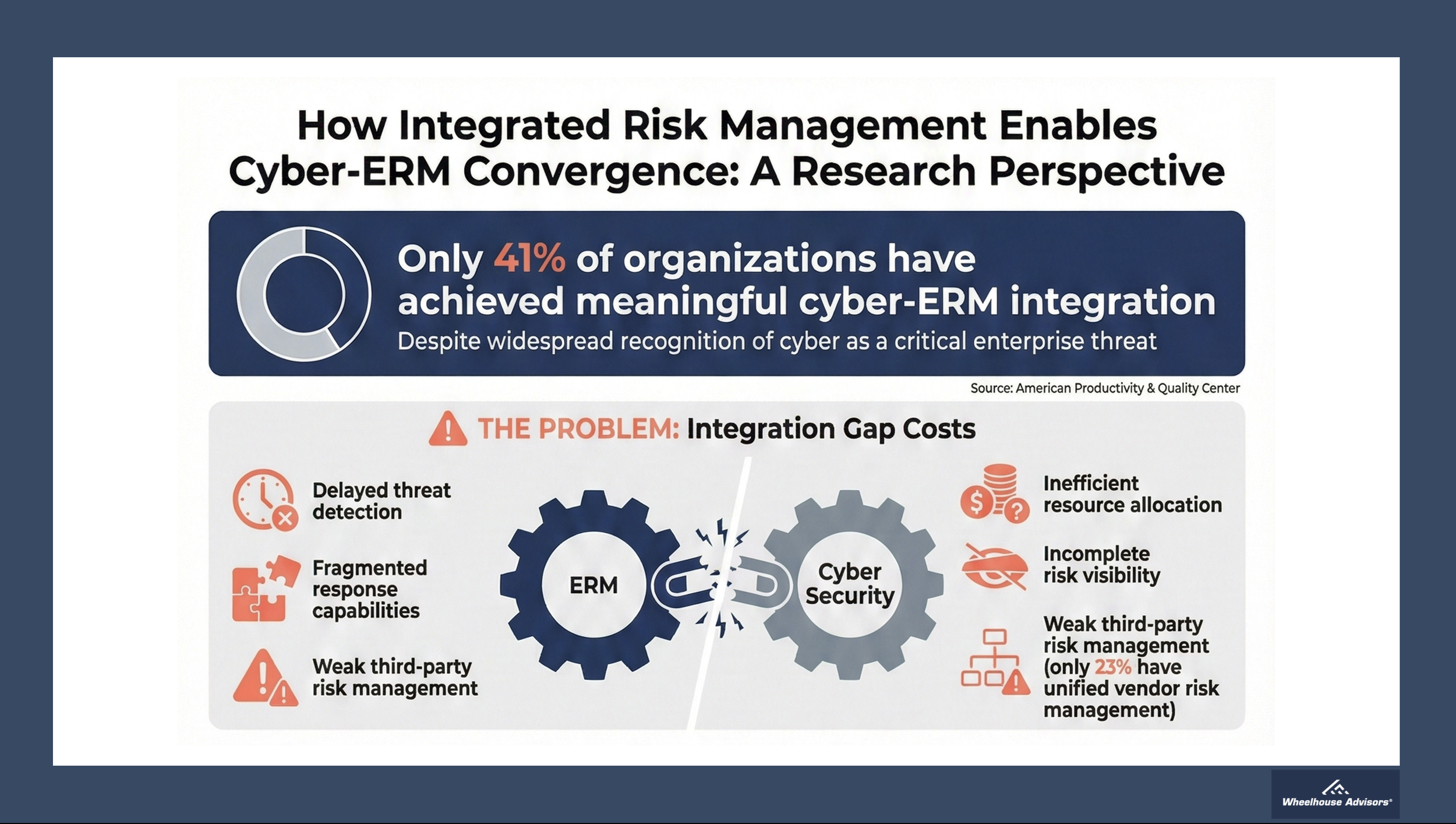

How Integrated Risk Management Enables Cyber-ERM Convergence

Recent research from the American Productivity & Quality Center reveals a sobering reality: only 41% of organizations have achieved meaningful integration between cybersecurity and enterprise risk management, and just 23% have unified third-party risk management. This gap persists despite widespread GRC platform adoption, revealing that compliance-first architectures cannot deliver the risk-first integration that cyber-ERM convergence requires. Integrated Risk Management provides the essential infrastructure to bridge this divide through its four-pillar framework: Performance, Resilience, Assurance, and Compliance.